Table of Content

LendingTree stands out from its competition due to its more than 1,500 partnered mortgage lenders and easy-to-use mobile app. Contact one of our top VA mortgage bankers today to learn more about our VA loan process. A VA-backed cash-out refinance loan can help you take cash out of your home equity.

It’s a statement or letter indicating how much, in principle, they will lend you. In addition to the criteria above, borrowers need to meet certain VA loan eligibility requirements to be approved. For one, the home needs to be used as a primary residence and occupied within 60 days after closing.

VA buyers can use their home loan benefit to purchase:

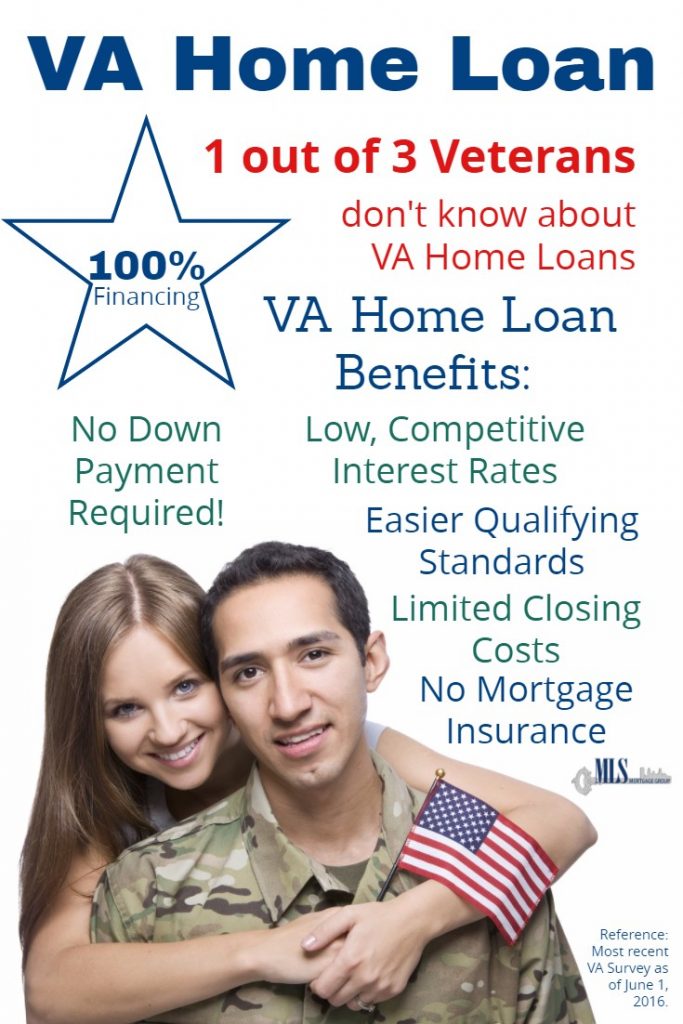

The VA funding fee can be paid for in a variety of ways and by no means has to be paid upfront. When you close on your VA loan, you can choose to pay the VA funding fee by rolling it into the total amount of your loan or pay the full amount at closing. The VA funding fees page has a rate chart that goes into greater detail as to how much you can expect to pay. A VA loan is a low or zero-down payment mortgage option offered to eligible veterans and active duty service members and their families.

With that being said, it is still up to your lender to determine how large of a mortgage you can borrow. Your mortgage banker will determine the size of loan you can afford by assessing your credit history, income, and any assets you may be holding. With VA loan requirements covered, it is important to mention there are still some restrictions as to exactly what types of properties you may purchase. If you meet the service minimums, you are entitled to the VA loan benefit.

Cover the earnest money deposit

Basically, how to pitch an offer that won’t alienate the owner but will have you paying the smallest amount possible. Don’t be tempted by a quick-fix purchase with the expectation that you can move again in a few years. Buying and selling a home is expensive and the real estate market unpredictable — you don’t want to do it more often than you absolutely have to. Through a state home buying program for first-time buyers or veterans, as well. Understand that this will increase your monthly mortgage payment.

They also typically offer lower interest rates and have lower closing costs. This makes them a great option for any veteran, but especially for first-time home buyers who may need extra help entering today’s competitive housing market. Acquiring a second VA loan does come with certain conditions. With most lenders, you must have a renter locked into a lease and a security deposit to offset your first VA loan mortgage payment.

When’s The Best Time Of Year

After so many failed offers, Anglim had no problem waiting another month to move in. Morford says many sellers also pause because VA loan appraisals typically come in slightly lower than general appraisals. But as Wemert points out, that’s just another negotiation opportunity for the contract. Again, a VA borrower could agree to cover any difference between the home’s appraisal and sales price. That’s the type of emphasis she places on customer service/satisfaction.

LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site . The VA home appraisal is required for a VA home loan and is arranged by your VA lender. As its name implies, earnest money indicates to the seller that you’re a serious buyer. You’ll get it back either as a deduction from your closing costs, or if your closing costs are covered by a third party, you’ll be refunded the amount.

Featured VA Loan Articles

The end goal is to have a solid Purchase and Sale Agreement that both parties are happy with. We here at National VA Loans put together this guide to outline the benefits of the VA home loan program. Read through the information on this page, and then give us a call. Most of the time, it’s also one of the largest financial investments you’ll ever make.

The VA will require some information and documents from you to apply for a COE so it is best to prepare your documents beforehand so that you can get through the application process smoothly. The most common is a service disabled veteran who is receiving VA compensation. You may be eligible for a refund of the VA funding fee if you are later awarded disability status from the U.S.

We also made sure that our picks are registered with the Nationwide Multistate Licensing System and Registry and meet the minimum certification requirements for mortgage lending. Guild is also a good choice for people who prefer in-person service, since they have branches in all but seven U.S. states. Notably, Guild services its loans, which is something that not all mortgage loan originators do. Navy Federal Credit Union is a financial institution that offers low rates and financial incentives to military families. See our VA loan guide to learn more about the type of loans available and the Veterans Affairs ’s service requirements. First, you will need to have a VA Home Loan Certificate of Eligibility .

©2022 American Pacific Mortgage Corporation.

So if you have some remaining entitlement, but not quite enough, consider making a down payment for 25% of the difference. If you don’t have enough entitlement remaining, you’ll have to put some money down. As a shortcut, just know that if you bought a low-priced home in a high-limit county, you may have enough remaining entitlement to buy again. Check your COE and talk to your lender to find out your exact remaining entitlement amount. If you’re in the market for a second VA loan, you must plan to live in your new home full-time, meaning at least six months out of the year. Understanding how to use a VA loan for a second home can make it easier for military servicemembers to move when they receive new orders.

Double-check all the figures and, in particular, make sure you aren’t being charged for a funding fee if you’re eligible for an exemption. Once it has all the required documentation, your lender submits your application to its underwriting department. This is the final step to officially approve your mortgage loan. It’s not uncommon for underwriters to request more information — called conditions — at this stage. Home inspections aren’t required to purchase a home, but they’re highly recommended — especially if you’re buying an older home.

Many lenders charge Veterans using VA-backed home loans a 1% flat fee (sometimes called a “loan origination fee”). Use your VA loan benefits, remain flexible about your price range and strike when the listing is hot. These can all add up to good home-buying strategy for Veterans and military families. The old adages “he who hesitates is lost” may really apply here. You might lose a home you love to another buyer is you wait too long.

No comments:

Post a Comment